If you're reading this, you're probably past the point of wondering whether you have a problem. The payments are missed. The letters from the lender are piling up. Maybe you've already received a court filing. This guide is written for that moment — not to scare you further, but to lay out exactly what's happening and what you can actually do about it.

The most important thing to know upfront: foreclosure in Illinois is a slow process. Unlike some states where lenders can move in weeks, Illinois is a judicial foreclosure state — meaning every foreclosure must go through the court system. That gives you time. Not unlimited time, but enough to make real decisions if you start now.

You are in active foreclosure. Illinois law requires lenders to file a Lis Pendens and serve you with a lawsuit before proceeding. If you've been served, your redemption window and available options are narrowing. Read this guide, then call us or a HUD-approved housing counselor today — not next week.

How Illinois Foreclosure Actually Works

Illinois uses a judicial foreclosure process — the only kind the state allows. This means your lender cannot foreclose on your home without first filing a lawsuit in circuit court, serving you with a summons, and obtaining a court judgment. This takes time and gives homeowners several legal protections that non-judicial states don't have.

Here's what the process looks like from a legal standpoint:

The Illinois Mortgage Foreclosure Law (IMFL)

The Illinois Mortgage Foreclosure Law (735 ILCS 5/15) governs every residential foreclosure in the state, including Peoria County. Under the IMFL, lenders must follow strict notice requirements, allow a reinstatement period, and provide a redemption period after judgment. These aren't just formalities — they're legal rights you can use.

The Right to Reinstate

Illinois law gives you the right to reinstate your mortgage — catch up on all missed payments, late fees, and lender costs — and stop the foreclosure in its tracks, up until 90 days after the lender serves the foreclosure complaint. After that window closes, reinstatement is no longer a legal right (though some lenders may still allow it voluntarily).

The Right of Redemption

Even after a court enters a judgment of foreclosure, you have a redemption period: 7 months from the date you were served the complaint, or 3 months from the date of judgment, whichever is later. During redemption, you can pay off the entire debt — not just the arrears, but the full balance — and reclaim the property. In practice, very few homeowners exercise this right because it requires full payoff, but it's there.

The Peoria County Foreclosure Timeline

This is what the process actually looks like on the ground in Peoria County, from first missed payment to completed foreclosure sale:

Peoria County has historically carried one of the higher foreclosure rates among Illinois metro counties — a reflection of the manufacturing job losses over the past two decades and the income volatility that leaves homeowners exposed when anything goes wrong. This isn't unusual or shameful. It's the economic reality of this community, and it's why knowing your options matters here more than in wealthier markets.

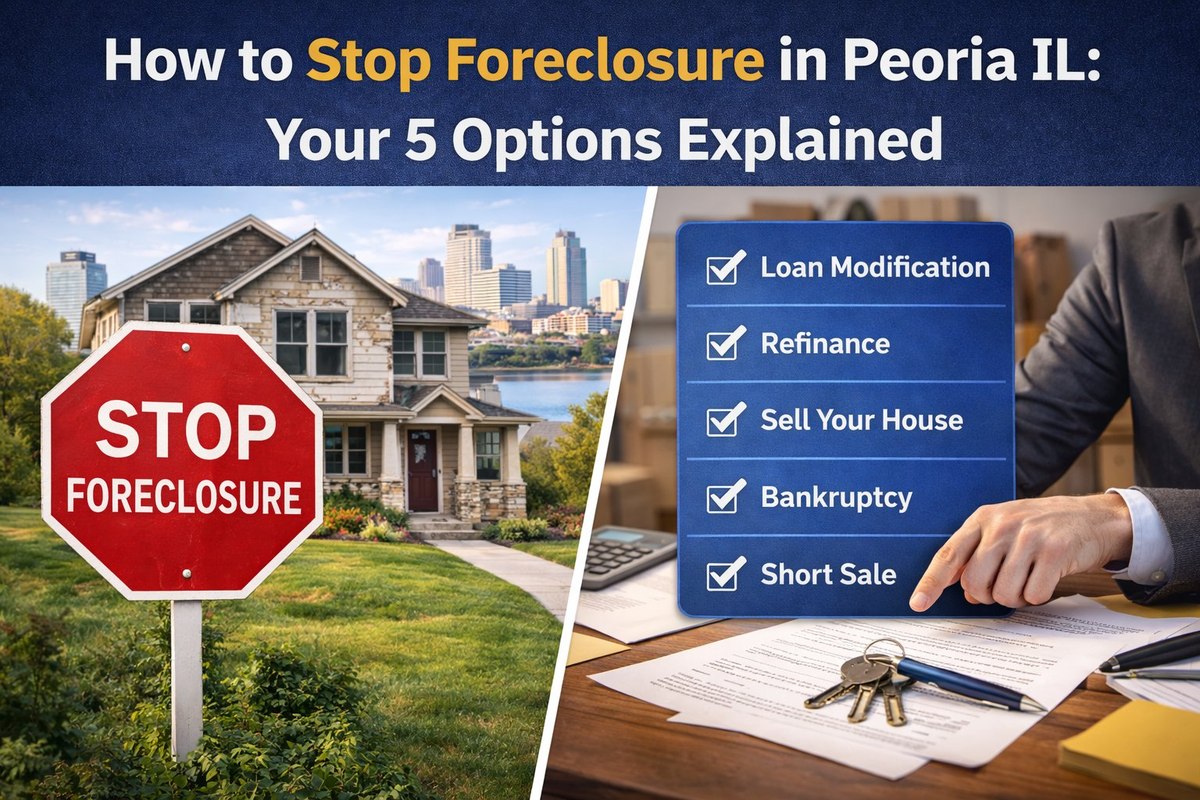

Option 1: Loan Modification

To qualify, you generally need to demonstrate a financial hardship, show that the hardship has been resolved or stabilized (new income, reduced expenses), and prove you can afford the modified payment. Modifications are not guaranteed — lenders can deny them, and the process often involves significant back-and-forth paperwork.

Free help in Illinois: The Illinois Housing Development Authority (IHDA) operates a Homeowner Hotline at 1-800-942-2028 staffed by HUD-approved housing counselors who can help Peoria homeowners navigate the modification process at no cost. This is a legitimate state resource — use it.

Pros

- You keep the home

- Can stop foreclosure completely

- Less credit damage than foreclosure

- Free assistance available through IHDA

Cons

- Approval not guaranteed

- Lengthy paperwork process

- Foreclosure continues during review

- Doesn't help if you can't afford any payment

Option 2: Forbearance Agreement

Forbearance works best when your hardship is genuinely temporary — a job loss, medical crisis, or income disruption that will resolve within months. If your financial situation is fundamentally broken (income permanently reduced, debt levels unsustainable), forbearance just delays the problem. Servicers are generally more willing to grant forbearance than modifications because the risk to them is lower.

Pros

- Fastest to arrange

- Stops foreclosure temporarily

- Buys time for a longer-term solution

- Relatively easy to request

Cons

- Doesn't solve the underlying problem

- Missed payments still owed at end

- Not a permanent fix

- Lender can still proceed if you don't follow up

Already Past the Early Stage?

If modification or forbearance isn't an option for your situation, a fast cash sale may be the cleanest path forward. We close in 14–21 days and have worked with Peoria homeowners at every stage of the foreclosure process.

Option 3: Sell to a Cash Buyer

If your home has equity — meaning it's worth more than you owe — you walk away with the difference after the mortgage payoff. If you're underwater (owe more than the home is worth), a cash buyer may not be able to cover the full balance without a short sale arrangement with the lender (see Option 4). But for most Peoria homeowners who bought their homes at reasonable prices and have made years of payments, some equity likely remains even in distress.

The key requirement: the sale must close before the foreclosure auction date. Even if you're months into the foreclosure process, a fast cash sale can still work. We've helped Peoria homeowners close in under 10 days when the auction was imminent.

Pros

- Stops foreclosure before it completes

- Closes in 14–21 days

- Preserves any remaining equity

- No repairs, no showings, no agent fees

- Foreclosure doesn't appear as "completed" on your record

- Works even with deferred maintenance or code violations

Cons

- Sale price below retail market value

- Must have enough equity to cover mortgage payoff

- Won't work if severely underwater without short sale

"Most homeowners don't realize they can sell their way out of foreclosure. They think the bank has already taken control. It hasn't — not until the auction is confirmed."

— our local team, Reliable Cash BuyersOption 4: Short Sale

Short sales in Illinois require the lender's written approval before the sale can close. This takes time — typically 60–120 days — because the lender must review the hardship documentation, order an appraisal or BPO (Broker Price Opinion), and formally approve the deal. During this period, the foreclosure case may continue in the background, so timing coordination is critical.

Illinois does allow lenders to pursue deficiency judgments after a short sale — meaning they can sue you for the forgiven amount. Some lenders waive this right in writing as part of the short sale agreement. Always get deficiency waiver language in writing before proceeding.

Credit impact of a short sale is significant but less severe than a completed foreclosure — typically a 100–150 point drop versus 100–160 for foreclosure, and the waiting period for a new mortgage is shorter.

Pros

- Option when you're underwater on the mortgage

- Less credit damage than completed foreclosure

- Shorter wait to buy again vs. full foreclosure

- Lender may waive deficiency judgment

Cons

- Lender approval required — not guaranteed

- 60–120 day timeline — may conflict with auction date

- Possible deficiency judgment if not waived

- Still significant credit damage

- Complex process — consider a real estate attorney

Option 5: Bankruptcy

Chapter 13 (Reorganization): Allows you to propose a 3–5 year repayment plan to catch up on mortgage arrears while continuing to make current payments. If you have a stable income and the financial discipline to sustain the plan, Chapter 13 can permanently stop a foreclosure and let you keep your home. It's the bankruptcy option most relevant to foreclosure prevention.

Chapter 7 (Liquidation): Discharges most unsecured debt but does not permanently stop foreclosure — once the stay lifts, the lender can resume. Chapter 7 can be useful if you want to walk away from the home without a deficiency judgment, since the discharge eliminates personal liability on the mortgage. But you will lose the property.

Bankruptcy is a serious legal step with long-lasting credit consequences (7–10 years on your credit report). It requires an attorney — the filing requirements for the Central District of Illinois are complex. This is not a DIY option. Contact a bankruptcy attorney in Peoria before considering this path.

Pros

- Immediate automatic stay stops all proceedings

- Chapter 13 can permanently stop foreclosure

- May discharge other debts reducing financial pressure

- Eliminates deficiency liability in Chapter 7

Cons

- Severe credit damage — 7–10 years

- Requires a bankruptcy attorney

- Chapter 13 requires income and 3–5 year commitment

- Chapter 7 does not save the home long-term

- Trustee reviews all assets and finances

The Most Important Thing: Act Now

Every option above has a window. Loan modifications work best before the lawsuit is filed. Reinstatement rights close 90 days after service. Redemption expires 7 months after service. Short sales take 60–120 days and need to close before the auction. Cash sales take 7–21 days but require equity to cover the mortgage payoff. Bankruptcy filings trigger an immediate stay — but serial filings lose that protection.

The single biggest mistake Peoria homeowners make in foreclosure is waiting. Not because they don't care, but because the notices feel overwhelming, the situation feels hopeless, and doing nothing feels like the path of least resistance. It isn't. Every week of inaction is a week of options narrowing.

Here's the practical action list, right now:

Call the IHDA Homeowner Hotline: 1-800-942-2028

Free HUD-approved housing counseling for Illinois homeowners. They can help you understand your specific loan situation, your timeline, and whether modification or forbearance is viable. No cost, no pressure.

Get a free cash offer to know your floor

Call us at (309) 322-2075 or submit your address at reliablecashbuyers.com. Takes 60 seconds and gives you a real number — what you'd actually receive if you sold today. Even if you don't end up selling, knowing that number clarifies your options.

If you've been served: respond to the lawsuit

Failing to respond to a foreclosure summons in Illinois results in a default judgment — and you lose the ability to contest anything. If you can't afford an attorney, Peoria-area legal aid organizations may be able to help. At minimum, file an appearance with the court to preserve your options.

Call your servicer before they call you

Servicers are required by law to discuss loss mitigation options before filing for foreclosure — but once the process is in motion, that obligation weakens. Call them, ask specifically about your loss mitigation options, and document every conversation (date, time, representative name, what was said).

We've Helped Peoria Homeowners Stop Foreclosure

Call us today — even if the auction date is close. A 14-day cash close has stopped foreclosure for homeowners who thought they were out of options. Zero cost to find out where you stand.

Frequently Asked Questions

How long does the foreclosure process take in Illinois?

From the first missed payment to a completed foreclosure sale, expect 12–18 months in Peoria County — sometimes longer if contested or if the courts are backlogged. Illinois is a judicial foreclosure state, meaning every case must go through circuit court. That's slower than non-judicial states, which is actually a benefit for homeowners — more time to act.

Can I sell my Peoria home to stop foreclosure?

Yes — and it's often the cleanest option. A fast cash sale can close in 14–21 days, pay off the outstanding mortgage balance, and stop the foreclosure before it completes as a legal event. The sale must close before the sheriff's auction is confirmed. If you have equity in the home — meaning it's worth more than you owe — you keep whatever remains after the mortgage payoff.

What is pre-foreclosure in Illinois?

Pre-foreclosure begins when you miss payments and your lender starts the notice process — typically after 90–120 days of delinquency. The formal pre-foreclosure period extends from that point until the lender files a lawsuit in court. This is your widest window of options: modification, forbearance, selling, or a short sale are all on the table.

What happens to my credit score in foreclosure?

A completed foreclosure typically drops your credit score 100–160 points and stays on your credit report for 7 years, preventing most conventional mortgage applications for 3–7 years. A short sale typically drops it 100–150 points with a shorter waiting period. Selling before foreclosure completes — even if you've missed payments — limits the damage significantly versus a completed foreclosure showing on your record.

Can I get a loan modification in Illinois?

Yes, but approval is not guaranteed. You'll need to document a qualified hardship, show financial stability going forward, and work through your loan servicer. Illinois has free HUD-approved counselors through the IHDA Homeowner Hotline (1-800-942-2028) who can help — at zero cost to you. This is a real resource, not a scam.

What is the Illinois redemption period?

After a court enters a judgment of foreclosure, Illinois law gives you a redemption period — typically 7 months from the date you were served the complaint, or 3 months from judgment, whichever is later. During this time you can pay off the entire loan balance and reclaim the property. Very few homeowners can exercise this right because it requires full payoff, but it's a legal protection unique to Illinois.